I wanted to add a little more from yesterday's post on Venture Capital.

The New York Times had an interesting piece about how a lot of start-ups (at least in the social media/Internet market) aren't generating revenue and would like to keep it that way.

When small start-ups I’ve spoken with do make money, they often find it difficult to recruit additional investment because most venture capitalists — and often the entrepreneurs they finance — are not interested in building viable long-term businesses. Rather, they’re interested in pumping up enough hype and valuation to find a quick exit through an acquisition at an eye-popping premium.

This is a very interesting trend. Here are a bunch of start-up companies with a bunch of investors waiting in line to fund them. And the entrepreneurs are trying to avoid concrete results, and focusing on speculative growth. The article used one obvious example. Instagram has $0 in revenue, but sold for $1 billion.

I think this pattern, in particular, will be a key cause of bubble growth (and bust) in this industry. One of the first things I learned in my Micro 101 class is the importance of the price system. Revenues are pretty good signaling devices for producers and investors. They show how valuable a good is to a consumer. No one really knows how much the big social websites (Facebook, Twitter, Google+, etc.) are valued by users, because they're all free!

This means that it's difficult for investors to know whether all these new start-ups are going to do well. Is there ever perfect information and predictability in a company? Of course not. But if the price of lead tennis balls was $0 - you would expect that investors would avoid investing in lead tennis ball factories. The only problem is that there's no way to tell which start-ups are making lead tennis balls and which are making the next Facebook.

I'm sure there has been more in-depth research on this. But the main point is that we should be wary of investments that aren't based off of much information.

As both a student and a young individual, I rely on the internet for a lot of the information I learn. I almost never think to browse my bookshelf or invest in an encyclopedia set when I'm looking for answers to questions. (Haha physical encyclopedias.) The Internet is essentially a gateway to the vast accumulation of human knowledge.

Now there has been a lot written about the affects of the new information age. Some think us youngsters don't think anymore and use the Internet like information-hungry parasites. Others think unlimited access to the Internet will lead to super brilliant children. And a lot of people are in the middle.

My fear is that we are breeding a new generation of Google Intellectuals.*

Allow me to explain. Young people are plugged into the Internet all the time. And use the Internet to learn and answer questions. In fact - I would argue that we use it so much, that we often forget that we might already have the tools to answer the question. We're becoming so dependent that we don't really need to use in-depth thinking to answer uncomplicated questions.

Of course, one could argue that not having to know the easy stuff just gives us more time to focus on more complex questions. It's kind of like saying that advanced math students can use calculators to focus on the theoretical topics.

That could be an answer, but I think it's a weak one.

Here's what I'm trying to get at - younger generations need to understand the value of consuming information more rigorously. (Using more System 2 in Kahneman's jargon.) We're so quick to gobble up random facts throughout the day, that we don't really take time to connect what we "learn" to the broader picture.

I think blogging helps you with that process. When blogging (especially about economics) you are forced to sit down and write about what you are learning. Often times you're even connecting different articles that you've read (through linking) to make a bigger point. This is especially true when you are writing about things that you care about.

Now that's how we should be learning!

Now does that mean that everyone should start blogging? Probably not. It requires a lot of patience and time, and a lot of people have neither. But taking the time to sit down, think, and write about a few topics will make you a much smarter person than Googling 100 different things a day.

*Google Intellectual (n) -a seemingly intelligent individual who accumulates their knowledge from random internet queries

Thought that was a pretty funny thing to hear in this interview.

They're also getting involved in the Venture Capital frenzy, investing in early-stage cloud companies.

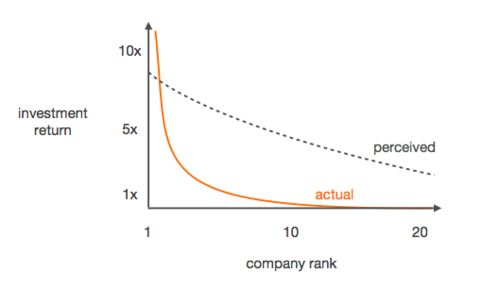

In all seriousness though, the idea of VC has been going around the blogosphere a lot. Peter Thiel gave a talk about how VC funds work. And showed this graph:

The basic principle is that for a VC fund, there are maybe one or two projects that actually make gains. A vast majority of the projects that are invested in tend to fail. . . I hope that this is something that VC managers (cough Winklevoss Twins cough) realize. Because it plays a big part in how the VC market works.

Particularly, I wanted to point out Noah Smith's post about a slump in VC returns since the burst of the Dot-com bubble. He references a paper that shows this graph:

The different lines are different data sets showing how well VC funds did relative to Private Market Equivalence (or how well the U.S. public stocks did in general). A PME of greater than 1 means that the VC investment did better than public stocks. If VC's fell below 1, then investors would for sure leave the market.

As you can see, we're in kind of a VC slump. Where gains haven't reached anywhere near the levels reached in the mid-1990s. Of course, there could be a number of reasons why that is.

Maybe the VC fund's of the 1990s got all the low-hanging fruit. That doesn't really seem to surprise me. There really hasn't been any HUGE payoffs from the internet apart from what we already have. Yes, we have social networks, but are they really driving that much economic value other than advertisements? It seems to me that Venture Capital does well when there are big breakthroughs in a certain industry, and there's a vacuum with how to apply those discoveries. In fact, in 2011, less than 30% of VC funds went to software and media industries, and more are going towards energy and biotechnologies. These are trends that I'm glad to see - considering payoffs might actually improve living standards a good deal. It'd be interesting to see what Tyler Cowen thinks in relation to his Great Stagnation theory.

But overall, I think the problem is that we haven't found some breakthrough way to apply big data or cloud computing. Hopefully these investments will help spur some of those discoveries...

This post is going to be very different from what I'm used to writing. But it's something that I've been thinking about (but has probably been elaborated on somewhere else).

I used to intern for Charlottesville Tomorrow, which is a non-profit news organization that reports on local politics, transportation, and community design issues in the Charlottesville area. For such a small organization (now three full-time employees, and one intern), it does some very impressive things when it comes to local journalism. For one - they manage an online wiki for all things Charlottesville, that contains user-generated information on everything from candidate bios and transportation projects to local restaurants and show venues. They engage with readers through Facebook and Twitter to get more involved in local affairs. And they often invest in visualizations of big transportation projects, so that citizens understand what's happening in their community.

Towards the end of my time there, I did a bit of reflecting on organizations like Charlottesville Tomorrow and the current state of journalism. Many people are lamenting over the dwindling budgets of professional media outlets as more and more people get their news from blogs, social websites, or other "informal" news outlets. It's a product of the information age! Today we get information from everywhere! Why wouldn't you expect the information specialists to go out of business?

Well I would argue that journalists are probably as important today as they've ever been - provided that they adopt a few new skills.

While we live in the age of information, some would say that we live in information overload. A lot of people haven't developed an effective way to sort through what's important and cast away what is just hollow ramblings on the internet. One important aspect of this is in the world of data. Open Data has been growing considerably since the Obama Administration started an initiative soon after taking office. "Big data" provides us with such valuable information, and has so many untapped opportunities.

And yet, in our lifetime, most of us will not (either through lack of time or lack of ability) interact with this open data movement, or use for our benefits. How would anyone even know where to begin?

This is where modern day journalists can come in. There is still a need for specialists to decipher and find important pieces of information for wider society, but it could be that finding those conclusions are just harder to find. Journalists' research can't just be confined to interviews, they have to dive into databases and other sources of "hidden information." Journalists need to start behaving like public researchers, and less like pundits.

And that's the basic idea. I'd love to hear other thoughts on this, though.

I've been thinking about this question, and Angry Bear posted a little about it. I think it's particularly interesting quandary when applied to suburban/urban communities. This post is really just meant to raise questions and drive discussion - rather than offering concrete proposals.

So what if everyone had driverless cars? Would highways work like public interfaces, where cars merged on and linked into one smooth transportation system? Or would traffic coordination just develop out of the technology itself? What if you could send your car places without you even being in it! (Taxi drivers should wouldn't like it.)

Of course, the applications are endless. But let's look at some practical applications. Assuming that the sensory coordination of cars was tuned to near perfection, you would expect the number of accidents to fall, because you wouldn't have the human error of recklessness.

Likewise, public transportation systems might benefit as well. If you could send your car back home, then you wouldn't have to deal with parking costs, and people may be more inclined to use the Metro to go to and from work.

I'll probably return to this concept in the future. Just an interesting think to ponder in the field of transportation economics.

Congressman Joseph Kennedy (D-Mass.) has an op-ed in the New York Times calling for a ban on oil speculation:

Today, speculators dominate the trading of oil futures. According to Congressional testimony by the commodities specialist Michael W. Masters in 2009, the oil futures markets routinely trade more than one billion barrels of oil per day. Given that the entire world produces only around 85 million actual “wet” barrels a day, this means that more than 90 percent of trading involves speculators’ exchanging “paper” barrels with one another.

This seems to be the new trend for Democrats. Not a bad political strategy, actually. Tying rising oil prices and Wall Street speculators together is a pretty smart way to stay on message.

However, it's very sloppy economics, so we'll have to focus on that part. (James Hamilton from Econbrowser has a good post on this too.)

Kennedy makes the point that a speculative catastrophe in the oil futures market would be much more devastating than one in the orange juice market, because there is a lack of available substitutes. On a basic level, that's exactly why we have speculators in the first place.

Speculators buy futures contracts on the expectation that prices will rise in the future. They buy oil today, when the price is relatively low, and sell in the future when supply is expected to fall. For consumers, the price may be higher, but they average out over a long period of time, rather than getting stuck in a hog market. If all the oil in Saudi Arabia disappeared tomorrow, and we knew it was going to happen, speculators would help avoid a complete meltdown of the economy.

That's not to say that oil speculation doesn't play any role in price volatility. Global shifts in demand are the main culprit, but oil speculation is expected to be the next biggest factor. Indeed, it seems as if speculation increases with increase in demand:

There's no point in taking out speculators for raising prices, when speculative prices are the result of growing global demand.

If it's a speculative bubble that Kennedy is worried about, then I don't think taking out speculators is necessarily the best solutions. For one, it's hard to determine how speculative bubbles rise because of the same reasons it's difficult to predict other financial bubbles. Predictions of where demand and supply will be in the future are based off of imperfect information.

Market Urbanism tweeted a report from McKinsey & Company that talked about America's reliance on urban centers for GDP. Interestingly, about 61% of GDP is attributed to small cities and rural areas.

That's huge! India also has the largest rural population, by far. China is on the fast track to urbanization. But why isn't India urbanizing as fast as other rapidly developing countries?

In comparison with China, India is still at relatively early stages of urbanization. Only 20 percent of the population lives in large cities, of which there are only 234. MGI estimates that large cities, scattered across the nation, will generate nearly 50 percent of the nation’s GDP by 2025.2 In India, it appears that state borders are limiting mobility, leading to an urban economic concentration in state hubs rather than city clusters across the nation. Moreover, India’s economic development policies have traditionally favored small-scale production and discouraged larger-scale operations in cities.

This is another factor slowing Indian urbanization that stands in contrast to both the United States and China where more mobile populations have moved in search of better jobs and other economic opportunities.

A paper from the Indian Statistical Institute says that one of the barriers to urbanization is capital utility in India's major urban centers:

Most of these cities using capital intensive technologies can not generate employment for

these distress rural poor. So there is transfer of rural poverty to urban poverty. Poverty

induced migration of illiterate and unskilled labourer occurs in class I cities addressing urban involution and urban decay.

India spends only $17 per capita annually on urban capital investment, compared with $116 per capita in China and $391 in the United Kingdom.

In addition, India's current urban spending varies dramatically according to the size of city. Tier 1 cities spend an average of $130 per capita each year, with 45 percent of this total on capital spending. However, owing to high general and administrative costs, most Tier 3 and 4 cities support per capita capital spending of only $1 currently.

So India's urban centers aren't very capital intensive relative to other nations, and capital spending depreciates relative to the size of the city. If capital investments were really strong deterrents for unskilled rural labor, then we might see urban growth on a smaller, regional basis, rather than from highly concentrated agglomeration.

Similarly, urban centers may not be doing so hot because of height limitations imposed by the government. If you can't build density, then you sprawl out and the livelihood of the urban center decreases. Refer to Edward Glaesar on this.

All together, India has simply not geared it's policy towards urbanization the same way China has. India needs to focus on its transportation and communication networks, because it's still on the path of urbanization, and can cause major infrastructural problems in the future.

I read this in two ways. The fact that financial earnings is still so far ahead of other sectors indicates the turbulence in Europe is pushing people towards American financial markets, and we still have a far way to go for recovery. (Both obvious points.)

It's still good to see that consumer discretionary, industrials, and technology are all doing moderately well.

1. Rates of growth stay in the range of 1 to 1.5 percent, see the work of Stock and Watson, top macro econometricians. Try redoing budget projections with those numbers.

2. Real rates of growth are higher than that, but they take the form of non-taxable pecuniary benefits.

3. Growth rates are acceptable, but more and more of economic growth is captured by private capital, which is difficult to tax for either mobility or political economy reasons.

4. The United States may need to fight a major war, or prepare to do so. (I do favor cutting the defense budget now, but we can’t be sure that cuts can last.)

5. The political economy of revenue hikes and/or spending cuts becomes or remains intractable. Buchanan and Wagner have been stressing this point for decades. A decision to borrow forty cents of a dollar spent, right now, may end up as more or less permanent, at least for as long as markets allow. Ezra’s excellent posts about how far “right” the Democratic Party has moved on taxes are along these lines.

6. Another major recession may arrive, perhaps from abroad.

7. Life expectancy goes up a few more years than we had thought, yet productivity for the elderly doesn’t rise in lockstep. You don’t have to think of that as “bad news,” but it still would be a major fiscal problem.

Health care costs are determined by a couple of things: demographic changes, induced demand, and perhaps most importantly, technology. There are people inside the medical system trying to reduce costs through more efficient uses of technology. Part of the ACA is to build systems (called Affordable Care Organizations in health industry jargon) around more efficient uses of care - which may include cutting back on expensive tests.

It'll be interesting to see how bundled payments play into this. Currently, patients pay for treatments the same way they order food off a menu (hat tip to Zeke Emanuel for the metaphor). Under a bundled payment system, patients will have access to a wide variety of treatments and procedures. Without the accountability systems, this could induce demand for more care instead of efficient care.

The short answer? It's almost impossible to tell at this point. Each state is still in the planning process of setting up their exchanges, and there's still debate whether the whole law will be thrown out by the Supreme Court.

Whatever insurance companies do not spend on health costs, they use for administrative purposes and profits. One of the key aspects of the Affordable Care Act is to make insurance companies raise their Medical Loss Ratios, or how much they spend on health costs. Also, each state will create an "exchange" that allows individuals to log on and look at each insurance plan all in one place.

Now the details of how these exchanges will be run is still pretty blurry, because each state decides how they want to set them up. Part of the goal is to reduce the marketing costs for insurance companies, since they'll have smaller administrative budgets.

For smaller companies, a lot of the marketing costs go to healthcare brokers; specialists who help groups or businesses navigate through the complexities of the insurance market and find the best plan for them. The "ideal" exchange would reduce the need for brokers, since all the comparisons (price, quality, medical coverages, etc.) will be on the website.

I asked Zeke Emanuel, one of the architects of health care reform, about this issue. (He was speaking at GMU today.) He thinks that brokers will still be around in the short-run. Businesses and large groups will still want the best information about what health plans are out there, and will use brokers to find that information. Of course, I'm sure there's concern for brokers to steer groups away from the exchange, since they are a competitive public good.

But marketing costs for small companies might not go down so quickly. When patients first go onto the exchange, there could be an advantage to having name recognition (i.e. being Blue Cross/Blue Shield) when being compared to other companies. Large companies may have enough marketing funds leftover to have an advantage over smaller companies in the exchange.

Another point: each exchange is being financed by a special tax put on the insurance companies involved. I can't imagine that a tax would cost more than current marketing/broker costs. Apart from a website and maintenance, and exchange should only include administrative costs. An ideal exchange would be one that reduces as most transaction costs, and provide near perfect information. State governments need to be keeping this in mind when they set up these markets.

Of course, this will all be looked at more closely when some of the data starts to come back.

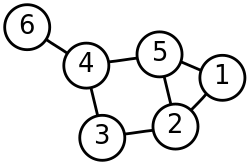

Graph Theory is a very simple way to show (visually) how different objects are related. It primarily consists of sets of edges and vertices that connect to make something like this:

Where the vertices are the numbered circles, and the edges are the lines connecting them. Of course, this example shows a very simple graph. Before you know it, they can start to look like this:

I'll be borrowing a large chunk of this post from a paper by Michael Konig and Stefano Battiston. I won't have time to cover the complex parts of the paper, but this will be a good preview of some of analysis that graph theory can help with.

The paper uses graph theory to analyze economic networks, which are just economic actors (firms, individuals, groups, etc.) that are organized to behave some way. Network economics differs from most neoclassical models, which use the perfect price competition models. The assumptions that people act individually and rationally are relaxed and analyzed more closely in economic network analysis.

In this post, we'll just look at network diffusion, and how knowledge can move from one person to another. Let's assume that vertices represent an individual, and the edges represent some sort of personal connection. (Note: Different lengths in the edges represent varying degrees of social connection. Small edges show that two people are closer than two people connected by a longer edge.) Therefore, closer edges are better ways of diffusing information than long edges.

The following equation is the average distance of all the edges. Where d is the distance between vertices i and j.

As you could assume, the lower average of the edge distance means that a network is more efficient at diffusing information. Konig and Battison cite a paper that shows that nearly 50% of all employment is facilitated through personal social circles. Using this kind of analysis is important in understanding how networks change and the impact of various inputs. (In this case, the diffusion of knowledge among a group of people.)

I would argue that network economics is becoming increasingly important as individuals become more interconnected through online social mediums. Similarly, this type of economic analysis could certainly be applied to urban environments, where interactions are becoming increasingly interrelated.

Part of what inspired me to write this blog is my ongoing frustrations with the GMU economics department. I'll write a more detailed post about this later, but for now I want to focus on a particular topic raised by my professor.

I'm taking Econ 306 (Intermediate Microeconomics) with Professor Walter Williams, who is a pretty well known economist and public intellectual throughout the nation. He is very intelligent and an excellent teacher. Nevertheless, I feel like I need to write about what he said to our class last week.

Here is a pretty good summary of what he told us:

"If you look at the history, from 1790 to 1920 the government did not respond to or took limited actions against recessions. These recessions would usually last from one to two years, and then naturally resolve themselves. However, if you look at recessions following 1929, they lasted much longer when the government tried to stop them. In fact, during the depression in 1920, the Harding Administration did barely anything, and the following decade was famously known as the "roaring '20s". So according to that track record, the government has done far more harm than good when it gets involved during economic downturns."

There's a few problems that I have with this conclusion.

1. This analysis is incredibly simplistic and sounds like something a politician would say on the campaign trail, not what a professional economist would say to his students. How could you quantitatively measure the effects of government intervention on recessions by simply looking at which downturns last longer? If you think that government intervention doesn't help the economy, fine. But don't tell your students that by looking at a timeline, you're going to find out why. Economics is about empirical explanations! With proofs, numbers, and logic!

2. I could have easily said that by not acting in 1920, developments in the '20s set the foundation for the Great Depression. Did it? I don't know. But the logic is just the same.

3. The recessions of a pre-globalized, pre-industrialized, pre-Wall Street America must be different from the recessions of the 1900s. So wouldn't it make sense that government policy would have a different affect on each one? Or maybe "modern" recessions have bigger impacts?

A lot of my friends majoring in a math or science like to tell me how economics isn't a "real science." If professors teach their students like this, then they are right.

Tyler Cowen elaborates on some of his views of higher ed:

To refer back to a distinction from the David Brooks column, we should not be trying to squeeze the entire economy into the shoebox of the dynamic but risky “Economy I.” For public choice reasons, as well understood by Karl Polanyi (an underrated public choice theorist if there ever was one), the polity requires some respite from Economy I, whether we like that or not. Read also this analysis by Interfluidity, which is one of my favorite blog posts of all time. Furthermore the more “sluggish” Economy II, by operating under different principles, often serves as a useful R&D lab for Economy I. Think MIT and Stanford, or note that Adam Smith ended up as a customs commissioner, as his father had been. Goethe and Bach worked for governments for much of their lives. It’s about balance and synergy, though it is perfectly fair to see contemporary Western Europe, especially in the periphery, as a region which has far too much Economy II and too little Economy I.

This is very similar to what I was saying in my previous post. Though state-run universities have their fair share of subsidies and "market inefficiencies", they're can still be stable incubators for research and innovation.

However, Cowen has additional comments on the plight of higher education:

The real problems are a few. First, successful state programs tend to stultify and decline over time, and if nothing else the danger is that health care costs will eat up state budgets. Second, the absolute returns to higher education (as opposed to the wage for not going) are not currently high enough to maintain the current fiscal structure of those institutions, furthermore those fiscal structures do not have so much “give,” due to tenure and various self-imposed cost inflexibilities. Third, although most state universities have relatively little explicit debt, they are implicitly massively leveraged through reliance on ongoing tuition boosts, ongoing enrollment boosts, and timely retirements, none of which can be counted on in the future.

Thomas Philippon, from NYU, has a new paper with this simple abstract:

Despite its fast computers and credit derivatives, the current financial system does not seem better at transferring funds from savers to borrowers than the financial system of 1910.

Now, before even reading the paper, I can already envision my Austrian economics professor starting his explanation of how the government has bogged down efficiency. Which - I would argue against. A lot of regulation has surrounded around making information about transactions more transparent.

Philippon points out that "compensation for financial intermediaries" is at 9% of GDP (an all time high).

Here is more:

Trading costs have decreased (Hasbrouck (2009)), but the costs of active fund management are large. French (2008) estimates that investors spend 0.67% of asset value trying (in vain, by definition) to beat the market.

In the absence of evidence that increased trading led to either better prices or better risk sharing, we would have to conclude that the finance industry's share of GDP is about 2 percentage points higher than it needs to be and this would represent an annual misallocation of resources of about $280 billions for the U.S. alone.

I'm not really in a place to give commentary in this issue. Though I'm glad it's being looked at. The real question is why? Trading is up substantially, which is a result of the democratization of finance (i.e. eTrade and such). But are people really better off? I guess the more important question is how much people think they are better off. Philippson finds that prices aren't any more informative of what's really happening in the markets. (I know, shocking.)

The Department of Justice sued Apple and five of the world’s largest book publishers on Wednesday, alleging that they colluded to increase the price of ebooks and cost consumers “tens of millions of dollars”.

The complaint, filed in the Southern District of New York, alleges that Apple and publishing executives agreed on a common response to Amazon’s pricing policy over phone calls, emails and meals in the “private dining rooms of upscale Manhattan restaurants”. Amazon, which had challenged the industry with a maximum ebook price of $9.99, is not named as a defendant.

Essentially, Apple representatives (including Steve Jobs) sat down with five other publishing companies to develop an "agency pricing model", where publishers sell their titles to Apple at a reduced price and Apple will receive 30 cents of every sale. One of the kickers is that the five publishers signed onto the "most favored nation" clause, where they agreed not to sell to other vendors (i.e. Amazon) at lower prices.

If you've taken Econ 101 - you might say that this sounds very cartel-esque, with all the talk of price fixing and colluding.

Right now under the so-called “wholesale” pricing model, the retailers of eBooks set the prices however low they choose. Clearly they cannot set these prices below the cost of production that has to be paid for the eBooks they peddle. But the marginal price for the production of an additional eBook is close to zero, so the retailers know that if they pay very little under this model the publishers will have no choice but to go along with the low prices. This strategy has let Amazon.com to price eBooks at around $9.99, which is a steep discount over the hard cover version.

In dealing with these matters, Apple proposed to all publishers that they shift to an agency model, whereby the publishers set their own prices and that Apple receive a 30 percent commission for the sales over its network. This same model could be offered to Amazon, which would allow it to compete on even terms with Apple, but would raise its prices, lower its margins and reduce its profits.

And there are a few reasons why this wouldn't fall under traditional antitrust violations.

For one, this new pricing model can work for Amazon too. It's not like Amazon is being locked out of this deal. As Epstein pointed out, the marginal cost of an eBook is so low, so Amazon/Apple (the big bad retailers) can charge as little as they want as long as it doesn't fall below marginal cost. The only problem is that when the price is so low there is increased disincentive to produce titles.

I think Epstein's biggest point is that this new model could have been proposed by a publisher, as well. And it's probably a more efficient system, where consumers are paying for the "real" price of the eBook. It just so happened that Apple (which has large influence over the market) started a trend that was bound to happen eventually.

As follow up conversation for Tyler Cowen's piece on America's export market, Ryan Avent talks briefly about higher education as one of America's most valuable exports.

A sector dominated by the state—state-run in some cases, merely subsidised and regulated in others—is, I think most Americans would agree, both a major contributor to American prosperity and one of America's most competitive industries on foreign markets, despite its glaring inefficiencies. What ought we to conclude based on this example?

Certainly, one could reasonably argue that the sector would be even better if state control were relaxed, monopolies broken up, subsidies curtailed, and market controls (like those on immigration) eliminated. But one also has to wrestle with how different the American economy would look if the state had never muscled public universities (including a broad network of technology-driven, extension-oriented schools) into existence.

For economists, higher education (and education in general) is difficult topic to tackle. There are thousands of variables that affect how colleges operate, and nearly 100 times as many variables that impact learning.

But while there are some concerns for the future of this industry, there are also big reason to celebrate. Are there inefficiencies? Certainly. Colleges that are primarily funded/managed by states can face substantial obstacles in how they manage and allocate their resources. But what about the benefits?

Ryan asks what the American college system would look like without state interventions, and links to a wikipedia article about Land-grant universities. These are universities originally designated by each state to receive the benefits of the Morrill Acts of 1862 and 1869. These universities were specifically designated to teach agriculture, engineering, and science as a response to the industrial changes of the time. I would argue that big investments in science education in the mid-1800s paid off. (And the full list of universities who opened under this act is pretty astonishing.)

Similarly, universities are becoming hubs for technological innovation in ways that the private sector is failing. For example, large pools of educated labor (eager undergrads) and capital investments (see charts below) are leading to substantial results in academic and applied research. No wonder these places are our biggest export!

So yes, American higher education has the red tape, the inefficiencies, the tenured professors, and the subsidies, but it also has so much more! It's not quite time to fret over this industry.

I received an email today linking me to a pretty cool video about consumption and the environment.

Starting around 11:00, Annie Leonard (narrator) starts talking about our behavior of purchasing goods then throwing them out 6 months later. It's a process called planned obsolescence, and Leonard claims that it was intentionally designed by corporations in the post-WWII era.

First off - what the heck is planned obsolescence?

It's actually a pretty interesting economic idea. It's the practice of producing goods that are designed to last for short periods of time before breaking down, or being replaced by superior models or designs. (Think about how new editions of textbooks frequently lower the value of past editions, or how Microsoft Word 2009 isn't compatible with the inferior Microsoft Word 2003.)

I won't really comment on how Leonards statement that planned obsolescence was "created" under the Eisenhower administration - because I don't have a clue of the history behind it.

But I WILL talk about the process, because there are certainly market structures that can create these conditions.

As an aside, it's important to not confuse planned obsolescence with just pure innovation. If companies are producing a good that provide much greater benefits than the model that was produced 6 months ago, then it's not planned obsolescence. It's innovation. And innovation is incredibly beneficial to consumers and shouldn't be seen as a corporate conspiracy to screw them over.

But that's not always the case.

Michael Waldman wrote a paper on this very issue in 1993, and explains some of the causes behind the behavior. (His model builds off of conclusions from the Coase-Bulow approach, with slight changes in the definition of planned obsolescence.)

The point of the analysis is to show that if the monopolist sells his output, then both from the firm's private standpoint and from a social welfare standpoint, his incentive will be too high to switch to technology B in the second period. The reason is that when he chooses which type of output to sell in the second period, he does not internalize how his choice affects the value of the units he sold in the previous period. Or to put the result another way, the monopolist faces a time-inconsistency problem; i.e., his actual technology choice in the second period is sometimes different from the choice he would make if he could commit to his second-period technology in the first period.

To put it more concisely - when a firm produces in time period 1, they aren't taking into account the affects of how it produces in time period 2.

Waldman writes that this leads to firm behavior that is less than socially optimal as a result of misplaced incentives.

So what is the policy solution to this situation? Waldman addresses that as well:

In a Coase-Bulow-type setting, it is true that a prohibition on leasing serves to reduce monopoly power. However, it is also the case that forcing the monopolist to sell may cause inefficiencies in production due to the monopolist's attempt to avoid the time-inconsistency problem. For example, the monopolist might respond by building less than the socially optimal level of durability into his output. The subsequent result is that even though a prohibition on leasing decreases monopoly power, it is still possible for social welfare to be reduced by such a rule.

If a monopoly was leasing a good (if consumers rented the good while the firm retained full ownership) than this behavior would be avoided, because the firm would avoid actions that would lower the costs of their assets (i.e. they wouldn't produce goods the devalue their current assets every few weeks). However, current monopoly regulations prohibit a monopoly to lease a durable good, which is a measure upheld by the supreme court to regulate monopoly power. So while allowing leasing may reduce planned obsolescence, it would be at the cost of reduced monopoly power. Bummer.

For now, college students should still expect to have to buy the new edition of their math textbook and be ready to throw their old copies out.

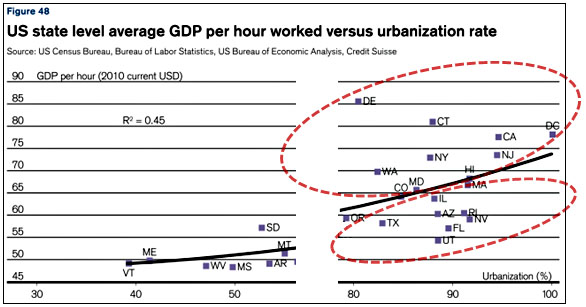

Alex Taborrok from Marginal Revolution posted yesterday about current trends in urbanization (a topic very near and dear to my heart) and was surprised by the strong correlation between GDP and urbanization rates as shown below (sorry for the bad formatting - had to make it big enough):

Kevin Drum from Mother Jones elaborated on some of this and Ryan Avents question: Why do some states have such large differences in GDP per hour but similar urbanization rates? (See graph below)

Drum pulled a conclusion from the original Credit Suisse report and wrote the following:

States that promote social mobility, discourage excessive income inequality, and are willing to invest in broad-based infrastructure, do well. Those that don't, don't.

But that's a pretty general cross-comparison to make. For many developing countries, urbanization has only been accelerating in the last 10 years, as compared to more developed countries that have been on a steady state of urbanization for decades. Such huge influxes of people have left many cities unable to support their populations, and therefore unable to tap into larger GDPs.

So it's hard to draw conclusions between U.S. states and countries when they have such different urbanization patterns. Time matters.

As to an answer why some states have higher GDP than others - it's a much more difficult question to answer. I think there we'll see many southern states continue to see their GDP rise as a result of population growth, but it's hard to say how effective their developing urban institutions will be.

Social network giant Facebook has bought Instagram – a profitless, two-year-old photo sharing website – for $1bn.

Instagram is a mobile sensation that counts Twitter co-founder Jack Dorsey among its backers. It has been downloaded by over 30 million people. When the Silicon Valley startup released a version for Android phone users this month, it was downloaded a million times in its first 12 hours.

Though Zukerburg mentioned that these kinds of acquisitions weren't likely to continue, that seems difficult to believe since Facebook's spending reports shows low R&D costs, implying a reliance on individuals to improve Facebook's quality.

So isn't there incentive for "social entrepreneurs" to create the next Instagram and sell it for high profits? And isn't there large payoffs for investors to finance them?

Not that it's necessary for analysts to flip out over one buyout, but it could be a situation where everyone wants to sell to the big rich giant. And this certainly isn't helping the Silicon Vally bubble debates.

One thing that all of these theories had in common— and, digressing again a little bit, one thing they share with several current theories of economic development — was that they were only about economics. Politics and institutions didn’t matter; only “economic fundamentals” mattered. The ones Rosenstein-Rodan emphasized were how much a society saved and how much foreign aid they got (which in the 1950s and 1960s was assumed to simply add to capital accumulation).

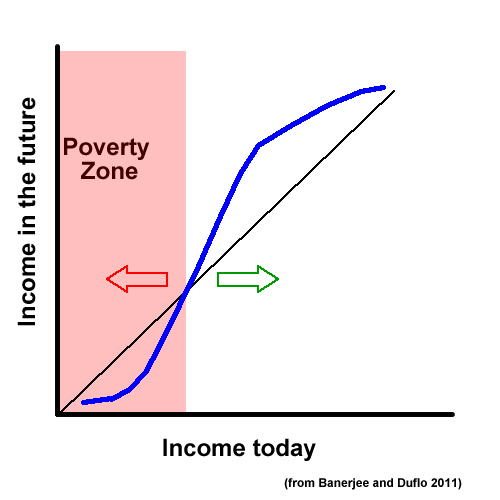

Big Push theory postulates that one firm's decision to modernize is dependent on other firms decision to do so, and that these firms will not modernize without a minimum amount of initial capital. (In other words - it's kind of like a poverty trap for firms.)

This graphs provide a good demonstration:

As you can see, this "S-curve" shows that in order to attain higher income in the future, there is a steep incline signifying the need for large initial investments. Of course, the ideas behind the Big Push theory isn't widely agreed upon and needs more robust analysis.

Daron Acemoglu and James Robinson's article is saying that the Big Push theory doesn't account for political or institutional barriers, which are especially important in developing countries where the large initial investments would be allocated.

This could be expanded. There's something to be said about how social media websites function as firms and the nature of their outputs.

Some general observations:

Facebook's "product" (access to the social network) is only as valuable as the number of users. And each user has his or her own unique social group. So in a bizarre way, the product is fine tuned to very specific interconnected sub-markets

There is a far amount written about Facebook's app economy. Some is here and here. Facebook is spending less on R&D, relying on outside developers. In the second link, it says Facebook is mimicking Apple's R&D model. The payoffs may not be as valuable for a company that is not producing replicable goods.

The new products that analysts keep talking about never actually leave the website. All new innovations (thus far) have remained on the profiles. Is there a diminishing marginal return for this pattern?

Overall it will be an interesting year for Facebook. There will be plenty of IPO analysis to go around, and I'm sure many anxious investors will it's much more valuable than it actually is.